In the last three decades, there have only been two years where both stocks and bonds have returned negative performances in the same year (using Australian index returns). Last year was the first year since 1994 that this has occurred.

We wrote in an earlier article, “…Asset allocation is the main driver of returns over time so this is where much focus should be paid to ensure an investor’s portfolio is commensurate with their risk tolerance.”

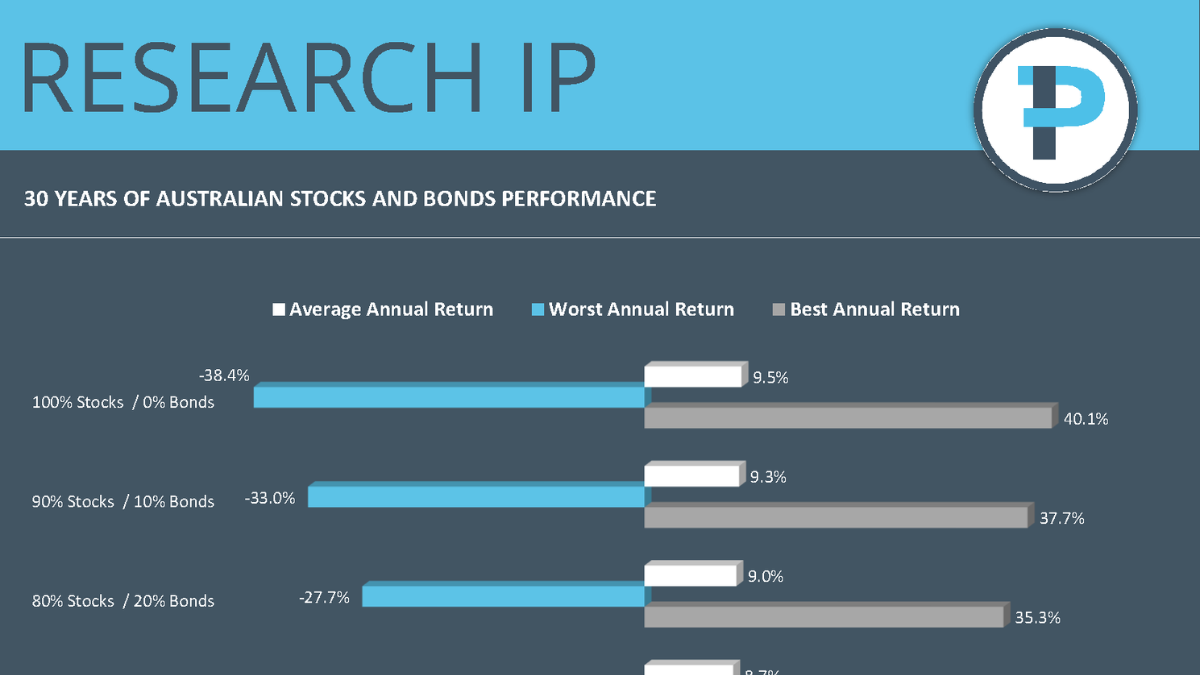

The graphic above and table below show the difference in portfolio returns between various combinations of stocks and bonds. If you had invested 100% of your investment portfolio in bonds then you would have averaged 5.8% per annum over the last 30 years. A portfolio of 60% stocks / 40% bonds would have averaged 8.4% per annum, and a portfolio of 100% stocks would have averaged 9.5% per annum. To put this in dollar terms the portfolios would have returned approximately $535,119 versus $1,115,835 versus $1,528,770 over the 30-year period.

However, the variation in returns in these 30 years would have been significant. Over the past 30 years, bonds have posted negative calendar year returns 13% of the time, a 60/40 portfolio 17% of the time, and stocks 20% of the time.

A 60/40 portfolio had its worst return in 2008, returning -17.1% during the Global Financial Crisis. A portfolio invested 100% in stocks would have returned -38.4% in its worst year (also 2008), whilst 100% in bonds would have returned -9.7% (in 2022). Not insignificant!

An investor’s time horizon for investing is enormously important to consider when deciding their appropriate risk profile and commensurate asset allocation split. When markets fluctuate more widely, the timing and order of returns are of more concern, particularly for investors that have liquidity needs from their portfolios.

We reiterate that ongoing governance and portfolio reviews are important to make sure the drivers of risk and return within the portfolio are appropriate for investors’ objectives.

Research IP’s key considerations for investors today:

- Be honest when assessing your risk profile.

- Stay the course; chasing investment performance often leads to being in the wrong asset class.

- Volatility has returned to the market.

- Inflation is likely to remain persistent, but at what level is not clear.

- Avoid the noise; it is an investor’s enemy, causing rash decisions to be made.

Where to from here?

Research IP currently has over 300 reports for managed funds available in the New Zealand market, as well as a range also available in Australia. The initial coverage also includes all default, balanced, and growth KiwiSaver offerings. Coverage of funds and data points is expanding daily.

- The RIPPL Effect reports are also available on interest.co.nz.

- You can find our research embedded at the point of sale on the new investment platform Flint Wealth.

- We announced a new partnership for Research IP in New Zealand with interest.co.nz at The RIPPL Effect – The future starts here – Research IP (research-ip.com)

Looking for something in particular or have some feedback? Please reach out to one of the RIPPL team

Research IP delivers high quality investment fund research and consultancy services to financial advisers, charities & NFPs and the broader financial services industry. Our experience spans well over 20 years working directly across the multiple facets of finance, so we understand the key drivers and challenges for managers, as well as the impact for investors and the broader industry.

We strive to give you the best information, so you can help your clients make better decisions, and feel more confident about doing business with you. We believe that not only can everybody win, everybody should.

Reach out to us today about your research and consulting needs, and how to make the data work for you, and your clients.

Would you like to see research on a Managed Fund? Then enquire here.

Photo credits: Research IP

Comments are closed